There are three major groups of transactions - purchase, sales and payment transaction, in other words expenditure, revenue and financial transactions.

- Purchase or expenditure transaction: money leaves the company's accounts;

- Sales or revenue transaction: money is added to the company's accounts;

- Payment or financial transaction: money is transferred from one account to the other.

Each transaction group has many different types (subcategories) that need to be monitored separately. For this reason, the information needs to be structured so that it is available in an easy-to-use form. For the structuring and reflection of accounting information, accounting accounts are used, which are the basic storage of data.

If you want to keep track of some information, for example the amount of cash, you need to keep a separate permanent record of this type of transactions. The accounting account will act as an accumulator of such information. Thus, the company creates a Cash account, where every transaction that increases or decreases the company's cash has been recorded. The information about any changes in the data should be recorded to the corresponding account. As a result, at any time you will have data on the amount of cash in the cash register.

An accounting account is a unique record for each type of transaction; it is the way accounting gets data organized, which allows you to sort, store and easily manage all the accounting records.

The accounting system (chart of accounts) of a firm can consist of tens, hundreds, or even thousands of accounts, depending on the size of the organization. Each of the accounts has its own number and name in the chart of accounts.

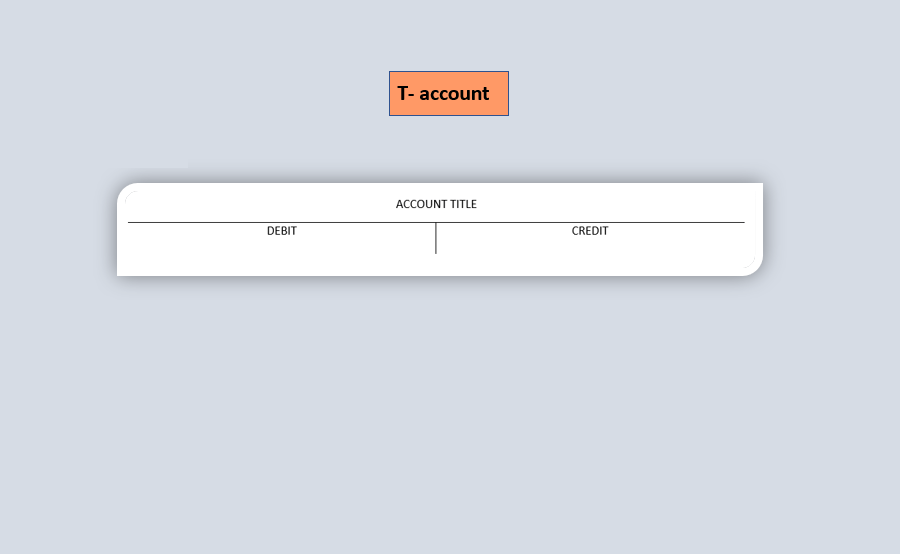

Visual structure of account has a shape like the letter T, it has two-columns in construction, where the left side is called the debit and the right side named credit. For different accounts, debits and credits may represent either an increase or a decrease. Debits increase the balance of assets and expenses, whereas credits decrease them. From the other side debits decrease the balance of liabilities, revenue and equity, whereas credits increase them.

When making an accounting record/entry (in Finnish, vienti), it is possible to talk about debiting (in Finnish, veloittaminen) the account when the entry is made on the debit side of the account, and crediting (in Finnish, hyvittäminen) when the entry is made on the credit side of the account.

| Account | |

| Debit | Credit |

The account title is a unique name assigned to an account depending on what needs to be tracked. If an account monitors the amount of cash, it is called a "Cash account". An account that tracks the amounts earned by employees is called a "Wages and Salaries account". Investments directly made by the owner are represented in the "Equity account". It is common for accounting account titles to be abbreviated by omitting the rest of the word "account" and the following names are used: Cash, Wages and Salaries, Equity, Accounts Receivable, Accounts Payable, Inventory, Administrative Expenses, Rent Expense, Equipment etc.

More information in the section "BUSINESS TRANSACTIONS RECORDING"