The chart of accounts, T-account, debit and credit, balance

The chart of accounts (COA) or the list of accounts is a clear and sufficiently detailed list of the accounts that explains the content of each account.

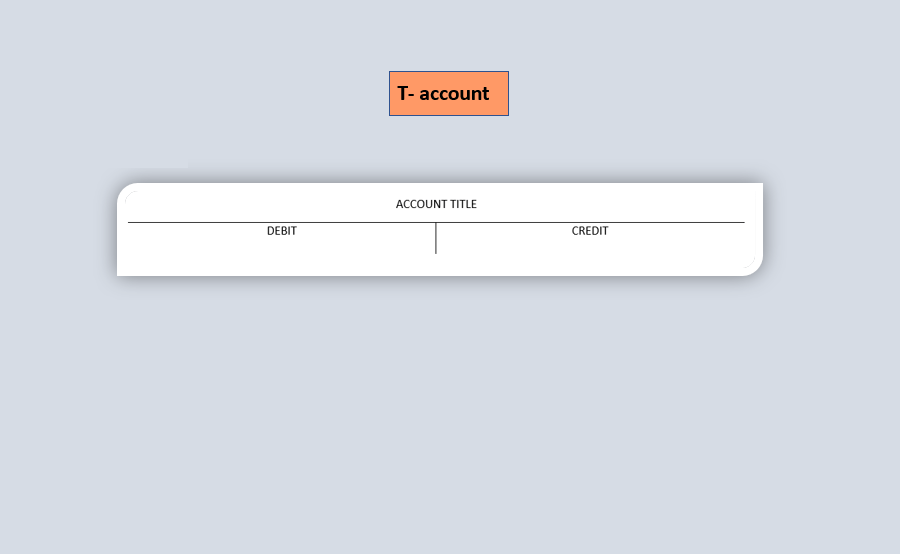

The T - account is a two-sided structure, where the left side is the debit (in Finnish: debet, veloitus, per) and the right side is the credit

(in Finnish: kredit, hyvitys, an). It is referred to T-account because it has the format of the letter "T". T-account is a useful tool for accountants, which helps to visualize a transaction. T-accounts are often used as a basic visual tool to understand how double-entry accounting works. It refers to the simplest format of an account that consists of debit side, credit side and the title of the account. See the slide

Every account has a name or title that is determined by the type of transaction, thus the events recorded to the account

are the same as an account content. Due to a change in the chart of accounts or other special reason,

the content of the account may be also changed.

The account has a balance, that is, the difference between debit and credit. The balance is either the credit balance

that is the sum of transactions (or the amount of entries) recorded on the credit side is greater than the sum recorded on the debit side; or the debit

balance when the sum of the debit entries exceeds the sum of the entries recorded on the credit side.

More information in the section "Accounts. What is an account in accounting?"

Accounting entry

On the basis of the source document, the company's accountant makes a record of a financial transaction into accounting books creating an accounting entry. Based on the entries, the company's financial statements are prepared, which include, among other things, the income statement and balance sheet. The data set of the accounting entry based on the supporting (source) documents have to provide the

following information:

- the date of the document

- the document's number

- the record to the chosen general ledger account

- the date of the record if it is different from the date of the supporting document

- the amount of the transaction

- in the case of sales and purchase invoices it is necessary to separate the VAT: show the information about VAT rate

and amount

Accrual or cash basis accounting can be used for financial transactions recording.

Taloushallintoliitto (in Finnish)

Audit trail or chain of records

There are three main financial statements that specify the financial accounting of a company: the income statement, the balance sheet, and the cash flow statement. The financial statements are prepared on the basis of different accounting entries. An audit trail is used to track down errors, changes and the causes of variances in records and, as a result, in the financial statements. It is used by both auditors and accountants.

An audit trail - is a continuous sequential chain of accounting records to trace the source of financial data. Daily transactions have to be recorded into accounting in a consistent way. Entries cannot be recorded into bookkeeping randomly and cannot be removed from records without any

supporting (source) documents.

The chain of records or audit trail must extend from the supporting documents (e.g. receipts,

invoices, and proofs of payment) to the financial statements and on the contrary, i.e. it should be easy to understand from which transactions the sum of particular entry shown in the financial statement consists of.

Accounting must be arranged so, that the audit trail / chain of records can be easily verified in either direction. This

rule also applies to the accounting when giving the reports to the authorities.

Taloushallintoliitto (in Finnish) and Accounting Act 1336/1997 (in English) / Kirjanpitolaki 30.12.1997/1336 (in Finnish), Chapter 2, Section 6

{kind=link}